Best Payment Processor for Small Business

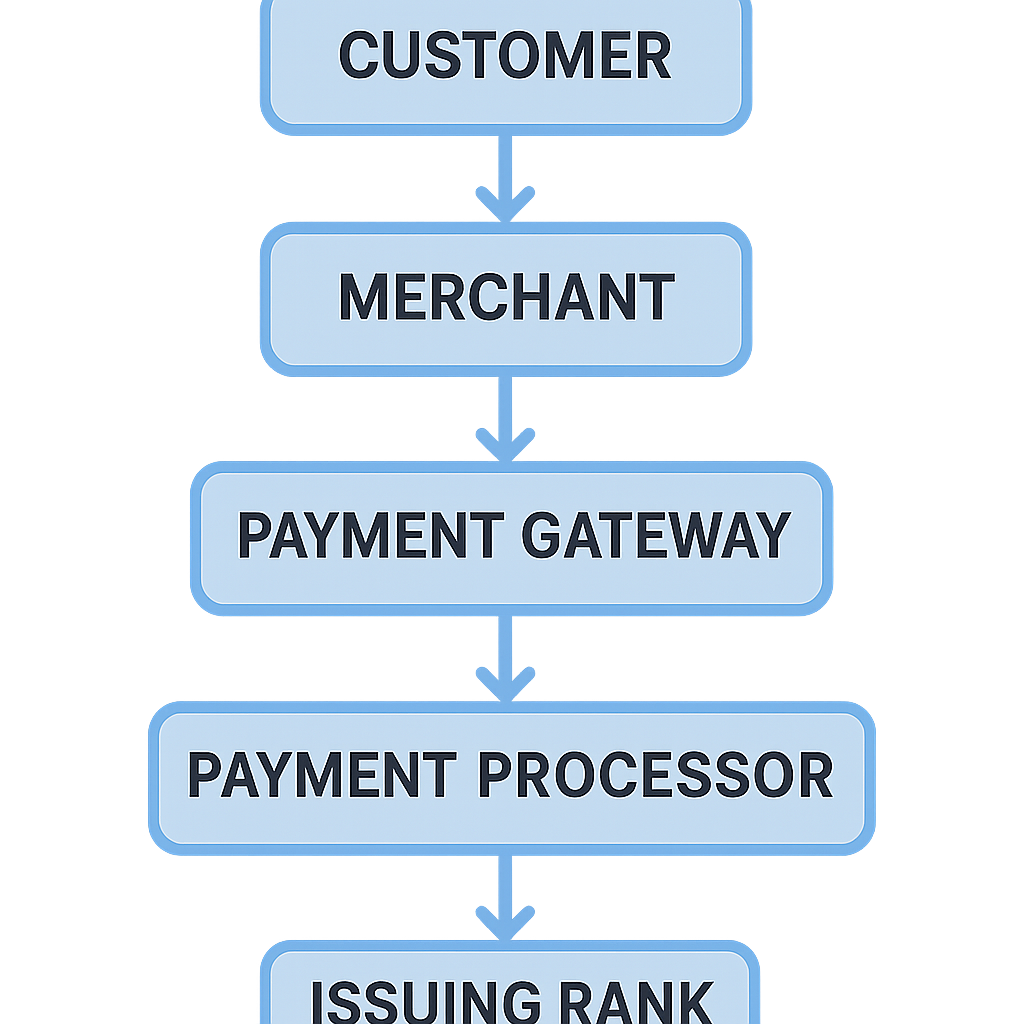

Payment processing involves managing transactions between your business and customers. A payment processor acts as an intermediary between your business, the customer’s bank, and your bank. It ensures secure and efficient transactions, whether in-store, online, or on mobile devices. As the digital economy grows, the role of payment processors becomes increasingly vital in accommodating new forms of payment and ensuring swift transaction execution.

In addition to facilitating transactions, payment processors provide critical services like fraud prevention and data security, which are paramount in maintaining customer trust. With cyber threats on the rise, selecting a processor with robust security measures can safeguard sensitive information and protect your business from potential breaches. Moreover, payment processors often offer analytics and reporting tools that give you insights into sales trends and customer behaviors, allowing you to make data-driven decisions.

Key Features to Look for in a Payment Processor

When selecting a payment processor, consider the following features:

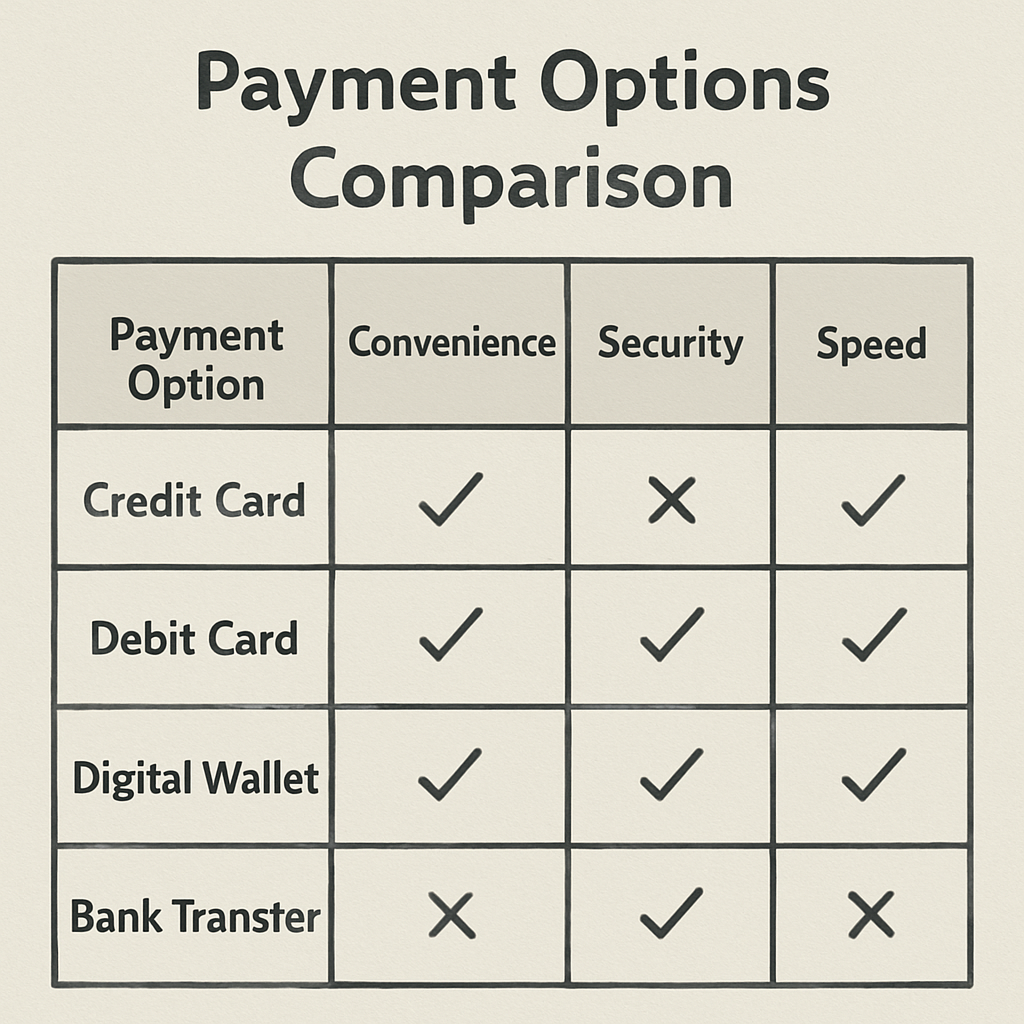

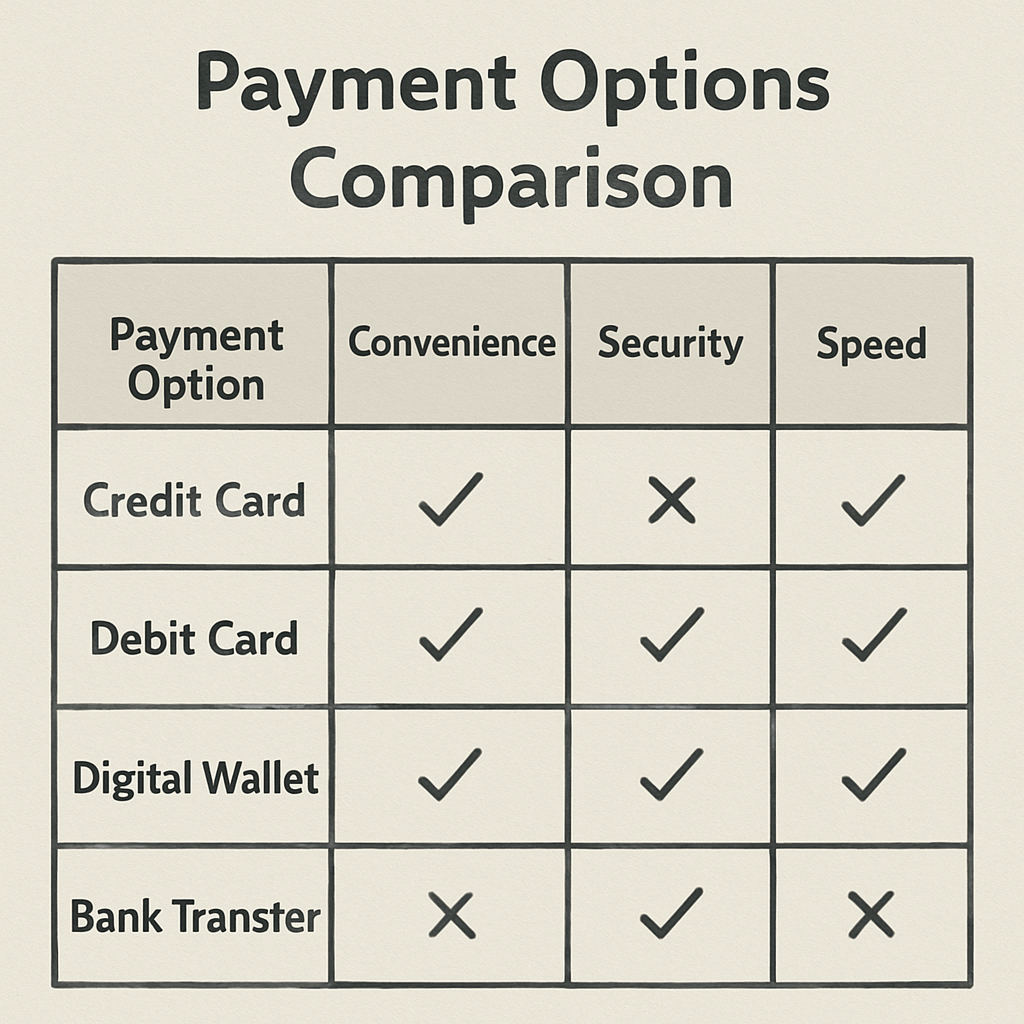

- Transaction Fees: Look for competitive pricing structures that suit your business model. Some processors offer flat-rate fees, while others may have variable rates based on transaction volume or business type. Understanding these costs is essential for maintaining healthy profit margins.

- Payment Options: Ensure the processor supports various payment methods, including credit cards, debit cards, and mobile payments. Offering diverse payment options can enhance customer satisfaction and increase sales by accommodating different customer preferences.

- Security: Choose a processor with robust security measures to protect your customers’ data. Look for features such as encryption and tokenization, which help prevent unauthorized access and reduce the risk of fraud. Security compliance, such as PCI DSS, is also a critical factor to consider.

- Integration: Ensure compatibility with your existing systems, such as your point-of-sale (POS) system or e-commerce platform. Seamless integration minimizes disruptions and enhances operational efficiency, allowing you to manage transactions more effectively.

- Customer Support: Reliable customer service can help resolve issues swiftly. Access to 24/7 support ensures that any technical difficulties or transaction disputes can be addressed promptly, minimizing potential impacts on your business operations.

Top Payment Processing Companies for Small Businesses

Selecting the best payment processor depends on your business needs. Here are some popular options:

1. Square

Square is a versatile payment processor favored by many small businesses for its ease of use and comprehensive features. It offers:

- Flat Rate Pricing: Square charges a straightforward fee of 2.6% + $0.10 per transaction for in-person payments, making it easy to predict costs. This transparent pricing model helps small businesses manage expenses without worrying about hidden fees.

- Free POS System: Square provides a free POS app, which can be customized to fit various business types. The app offers inventory management, sales tracking, and customer engagement tools, making it an all-in-one solution for business operations.

- Mobile Payments: With Square, you can accept payments on-the-go using their mobile card reader. This flexibility is ideal for businesses that operate at events, markets, or pop-up shops, allowing them to capture sales opportunities anywhere.

2. PayPal

PayPal is a well-known name in payment processing, offering solutions for both online and in-store transactions. Its features include:

- Global Reach: Accept payments from around the world, expanding your customer base. PayPal’s global network makes it easy for small businesses to tap into international markets without the hassle of currency conversion.

- Secure Transactions: PayPal is renowned for its secure payment processing and buyer protection. This reputation can help build customer trust, especially for new businesses looking to establish credibility.

- Flexible Payment Options: Customers can pay using credit cards, PayPal balance, or through a linked bank account. This versatility caters to a wide range of customer preferences, potentially increasing conversion rates.

3. Stripe

Stripe is ideal for e-commerce businesses, offering a developer-friendly platform that supports a variety of payment methods. Key features include:

- Customizable Solutions: Stripe’s API allows businesses to tailor the payment process to their needs. This flexibility is beneficial for businesses with unique payment requirements or those looking to integrate complex systems.

- Subscription Billing: Ideal for businesses offering subscription services, with built-in tools for managing recurring payments. Stripe’s automated billing and invoicing features simplify the management of ongoing customer relationships.

- Advanced Security: Stripe uses advanced encryption to secure transactions. Their commitment to security includes features like machine learning-based fraud detection, adding an extra layer of protection for your business.

4. Shopify Payments

For businesses using Shopify as their e-commerce platform, Shopify Payments offers seamless integration. Benefits include:

- No Transaction Fees: Avoid additional transaction fees when using Shopify Payments. This can significantly reduce costs for businesses processing a large volume of sales.

- Multi-Currency Support: Cater to international customers with multi-currency acceptance. This feature can enhance the shopping experience for global customers, potentially increasing international sales.

- Fraud Prevention: Built-in fraud detection tools to protect your business. Shopify Payments’ security measures work to prevent chargebacks and fraudulent transactions, safeguarding your revenue.

Tap Simple

-

No-fee payment processing powered by a cash-discount model, helping merchants eliminate traditional credit card fees.

-

Offers both software and hardware payment solutions for small businesses.

-

Accepts EMV chip, magstripe, and NFC/contactless payments.

-

Includes a “Pay Anywhere” mobile app, virtual terminal, and smart terminals like the Smart Flex.

-

Centralized Payments Hub for managing:

-

Sales

-

Employees

-

Inventory

-

Invoices

-

Reporting

-

-

Tailored for field service providers, small retailers, and local service businesses.

-

Focused on providing simple, transparent, and low-cost payment solutions without hidden fees.

Mobile Payment Systems for Small Businesses

by hellooodesign (https://unsplash.com/@hellooodesign)

Mobile payment systems are becoming increasingly popular, providing flexibility and convenience. Here are some leading mobile payment options:

1. Apple Pay and Google Pay

These digital wallets allow customers to pay using their smartphones. Benefits include:

- Quick Transactions: Customers can complete purchases swiftly using their phone’s contactless capabilities. This speed not only enhances customer satisfaction but also reduces wait times, improving the overall shopping experience.

- Security: Both Apple Pay and Google Pay use tokenization to keep payment information secure. This technology replaces sensitive card data with a unique identifier, minimizing the risk of data breaches.

- Wide Acceptance: Many payment processors and POS systems support these mobile payment options. This broad acceptance makes it easy for businesses to adopt mobile payments without extensive infrastructure changes.

2. Zelle and Venmo

For peer-to-peer transactions, Zelle and Venmo offer simple and fast payment solutions:

- Instant Transfers: Funds are transferred quickly, often in real-time. This immediacy is beneficial for businesses looking to improve cash flow and maintain operational liquidity.

- User-Friendly Apps: Both platforms offer intuitive apps for seamless transactions. Their ease of use encourages adoption among customers who prefer hassle-free payment methods, potentially broadening your customer base.

How to Set Up Online Payments for Your Small Business

Setting up online payments is essential for businesses looking to expand their reach. Here’s a step-by-step guide:

Step 1: Choose a Payment Processor

Select a processor that aligns with your business goals, considering factors like fees, integration, and payment options. Research various providers to compare features, costs, and customer reviews to make an informed choice that suits your needs.

Step 2: Integrate with Your Website

Ensure your chosen payment processor integrates smoothly with your website or e-commerce platform. Most providers offer plugins or APIs for easy integration. Test the integration thoroughly to ensure that it functions as expected and provides a smooth checkout experience for your customers.

Step 3: Secure Your Payment Process

Implement security measures, such as SSL certificates and PCI compliance, to protect customer data and build trust. Educate your team on security best practices and regularly update your systems to mitigate potential vulnerabilities.

Step 4: Test the Payment System

Conduct thorough testing of your payment system to ensure smooth operation and address any issues before going live. Involve real users in testing to gather feedback and make necessary adjustments to enhance usability and reliability.

Conclusion

Choosing the best payment processor for your small business is a critical decision that can impact your operations and customer satisfaction. By understanding your business needs and exploring the options available, you can find a payment processing solution that supports your growth and success. Consider factors such as transaction fees, payment options, security, and customer support when making your choice.

With the right payment processor, you can offer customers a seamless and secure payment experience, positioning your business for success in today’s competitive market. As you navigate the complexities of payment processing, remember that the right choice will not only facilitate transactions but also enhance customer trust, drive sales, and contribute to your business’s long-term success.

{kind=link}

{kind=link}

{kind=link}